Frequently Asked Question 4

What will my monthly mortgage payment be?

Principal and Interest – Monthly amount of your mortgage payment that is applied to

your loan balance and interest charges for your loan.

Property Taxes – If you have an escrow impound account (required on FHA, VA, and Conventional loan with less than a 20% down payment) a portion of your total monthly payment will be placed in an escrow impound account. This escrow impound account is used to pay your property taxes and homeowner’s insurance when they are due. Property taxes are normally about 1.25% annually, based on the purchase price of your home. Property tax rates vary from community to community, but 1.25% or less is about the average in Southern California.

Homeowner’s Insurance – All home loans require homeowner’s insurance, this insures your home (for you and the lender) against damages, theft, lawsuits, etc. This is either paid via your escrow impound account or by you when the premium is due (depending on whether or not you have an escrow impound account). Many homeowners enjoy having an escrow impound accounts for this reason: it requires the homeowner to set aside a portion of money each month for their homeowner’s insurance premium and property taxes, verses having to come up with the money in a lump sum when those items are due.

Mortgage Insurance – There are 2 different types of mortgage insurance: FHA Mortgage

Insurance (MIP) and Conventional Mortgage Insurance (MI).

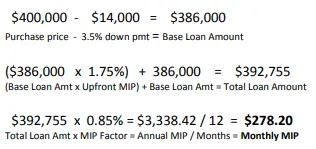

FHA Mortgage Insurance – Is applied to all FHA mortgages, regardless of the down payment amount. The FHA mortgage insurance (MIP) factor is calculated based on the percentage of your down payment. A 3.5% down payment gives you an MIP factor of 0.85%, while a 5% or greater down payment gives you an MIP factor of 0.80%.

With FHA loans, there is also an Upfront MIP which is added to your base loan amount when you receive the loan. This Upfront MIP is 1.75% of your base loan amount and is paid to FHA (Federal Housing Administration). The upfront MIP is used by FHA to keep the FHA loan program working and able to continue. Here is how the MIP factors works for the Upfront MIP and the monthly MIP (assuming a 3.5% down payment and 30 year fixed loan):

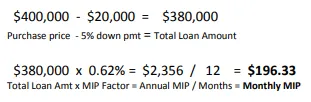

Conventional Mortgage Insurance – One of the main benefits to a Conventional loan

with mortgage insurance (compared to FHA) is there is no upfront mortgage insurance

with a conventional loan, just the monthly mortgage insurance. The down side is conventional loans have stricter guidelines for qualifying and the mortgage insurance is based on your credit score as well as the percentage of down payment you make (720 FICO score with a 10% down payment will have a much lower monthly mortgage insurance premium than a borrower with a 620 FICO score putting only 5% down).

Another difference with conventional mortgage insurance is that it is offered by private

mortgage insurance providers, just like auto and home insurance is provided. Regardless of the provider, the calculation for determining your monthly mortgage insurance premium is the same and the MI factors are relatively the same amongst providers. Here is how conventional monthly mortgage insurance works (assuming a 5% down payment and 720 FICO score):

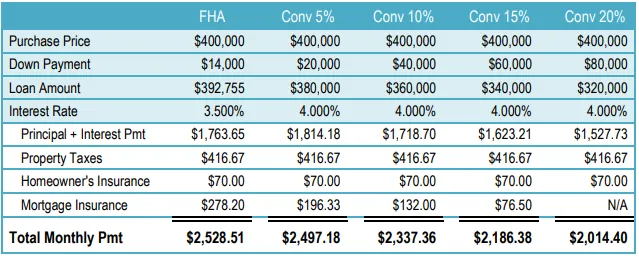

As you can see, if you have a decent FICO score and 5% down payment or more, choosing a

conventional loan will save you money each month with a lower mortgage insurance premium, in addition to not having an Upfront MIP (required on FHA loans). Conversely, if you have a lower FICO score (usually 660 or lower) and/or are putting less than a 5% down payment, private mortgage insurance rates increase dramatically. It is my job to help my clients review all their available options and help them decide which is best for their purchase or refinance needs.

Your total mortgage payment: FHA vs. Conventional (based on 720 FICO):

How Much Will I Qualify For?

This is the big question… possibly the biggest! Without knowing your specific FICO score, work history, annual/monthly income, and ability to make a down payment, it is impossible to say how much you will qualify for. But I have been able to help even the hardest to finance clients purchase a home within 6 to 12 months. So don’t count yourself out without calling me first! Realistically, if you’ve had a job for 12 months or more, have a decent credit score (580 or higher), and have some money saved for a down payment/gift money for a down payment: I CAN HELP YOU RIGHT NOW! If you need help getting to that point, please call me so we can make a game plan and get you ready to buy a home in the near future (3-12 months)!